Buy Now, Pay Later (BNPL) offers pet owners flexible payment options with no immediate interest, making it easier to purchase premium pet products without financial strain. Traditional credit often comes with higher interest rates and longer repayment periods, which can lead to increased overall costs for pet supplies. BNPL services enhance customer experience by simplifying checkout processes and promoting responsible spending for pet care essentials.

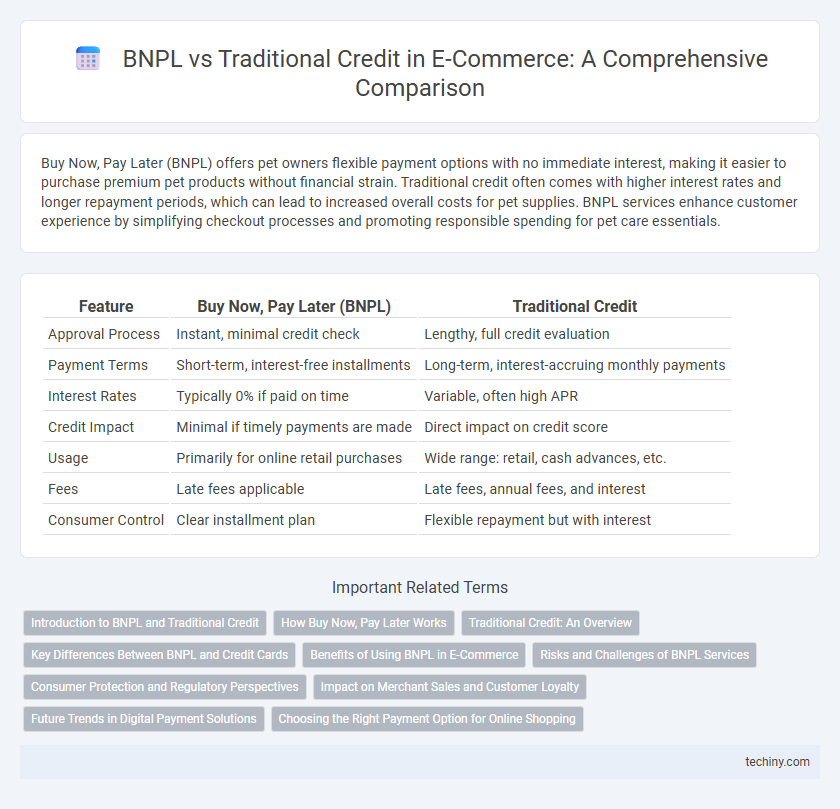

Table of Comparison

| Feature | Buy Now, Pay Later (BNPL) | Traditional Credit |

|---|---|---|

| Approval Process | Instant, minimal credit check | Lengthy, full credit evaluation |

| Payment Terms | Short-term, interest-free installments | Long-term, interest-accruing monthly payments |

| Interest Rates | Typically 0% if paid on time | Variable, often high APR |

| Credit Impact | Minimal if timely payments are made | Direct impact on credit score |

| Usage | Primarily for online retail purchases | Wide range: retail, cash advances, etc. |

| Fees | Late fees applicable | Late fees, annual fees, and interest |

| Consumer Control | Clear installment plan | Flexible repayment but with interest |

Introduction to BNPL and Traditional Credit

Buy Now, Pay Later (BNPL) enables consumers to purchase products immediately while spreading payments over time without interest, enhancing affordability and cash flow management. Traditional credit involves borrowing funds from financial institutions with structured repayment schedules and often incurs interest and fees. BNPL's streamlined approval process contrasts with the credit checks and eligibility criteria typical of traditional credit, offering a frictionless checkout experience for e-commerce shoppers.

How Buy Now, Pay Later Works

Buy Now, Pay Later (BNPL) allows consumers to split purchases into interest-free installments, providing immediate possession of goods without upfront full payment. This model leverages real-time credit approval based on minimal data, enhancing convenience and accessibility compared to traditional credit cards that often require detailed credit checks and charge interest. BNPL systems integrate seamlessly with e-commerce platforms, offering flexible payment plans that drive higher conversion rates and average order values.

Traditional Credit: An Overview

Traditional credit in e-commerce offers consumers the ability to purchase goods immediately while repaying the balance over time with interest, typically through credit cards or store financing. This method often involves credit checks, fixed interest rates, and monthly minimum payments, which can impact credit scores if not managed responsibly. While traditional credit provides flexible purchasing power, it may result in higher long-term costs compared to alternative financing options like Buy Now, Pay Later (BNPL).

Key Differences Between BNPL and Credit Cards

Buy Now, Pay Later (BNPL) offers short-term, interest-free installment plans designed for immediate online purchases, contrasting with traditional credit cards which provide revolving credit with variable interest rates and longer repayment periods. BNPL services typically require minimal credit checks and promote fixed payment schedules, whereas credit cards involve comprehensive credit assessments and flexible spending limits. Merchants benefit from higher conversion rates with BNPL, while credit cards often incur greater fees but offer rewards programs and broader purchasing power.

Benefits of Using BNPL in E-Commerce

Buy Now, Pay Later (BNPL) offers e-commerce shoppers flexible payment options without interest or hidden fees, enhancing purchasing power and reducing cart abandonment rates. Unlike traditional credit, BNPL approvals are often instant with minimal credit checks, enabling quicker and easier access to funds. Merchants benefit from increased average order values and improved customer satisfaction by integrating BNPL solutions at checkout.

Risks and Challenges of BNPL Services

Buy Now, Pay Later (BNPL) services pose significant risks including higher default rates and lack of regulatory oversight compared to traditional credit, increasing financial vulnerability for consumers. These services often encourage impulsive spending without sufficient credit checks, leading to accumulated debt and potential credit score damage. Merchants face challenges in managing cash flow and fraud prevention due to delayed payments and limited risk assessment protocols in BNPL models.

Consumer Protection and Regulatory Perspectives

Buy Now, Pay Later (BNPL) services offer flexible payment options but often lack the stringent consumer protection measures found in traditional credit systems, raising concerns about transparency and debt accumulation. Regulatory bodies are increasingly scrutinizing BNPL providers to implement standards akin to those governing credit cards, emphasizing clear disclosure, affordability assessments, and dispute resolution mechanisms. Enhanced regulation aims to balance innovation in e-commerce financing with safeguarding consumers from predatory practices and over-indebtedness.

Impact on Merchant Sales and Customer Loyalty

Buy Now, Pay Later (BNPL) solutions boost merchant sales by increasing average order values and conversion rates compared to traditional credit methods, which often involve complex approval processes and higher decline rates. BNPL enhances customer loyalty through seamless, interest-free installment plans that improve the shopping experience, encouraging repeat purchases and brand affinity. Merchants leveraging BNPL benefit from higher customer retention and increased lifetime value, contrasting with the slower, less flexible credit options that may deter frequent engagement.

Future Trends in Digital Payment Solutions

Buy Now, Pay Later (BNPL) services are reshaping e-commerce by offering flexible installment plans that enhance consumer purchasing power without immediate credit checks, contrasting traditional credit's reliance on interest and credit scores. Emerging digital payment solutions integrate AI-driven risk assessment and blockchain technology to improve transaction security and speed, positioning BNPL as a preferred option among younger, tech-savvy shoppers. Future trends indicate a convergence of BNPL with embedded finance and seamless omnichannel experiences, driving higher conversion rates and personalized payment methods across global markets.

Choosing the Right Payment Option for Online Shopping

Buy Now, Pay Later (BNPL) offers flexible, interest-free installments that appeal to budget-conscious online shoppers, contrasting with traditional credit cards that often involve interest charges and credit checks. Understanding factors such as payment schedules, fees, and credit impact is crucial when selecting between BNPL services like Afterpay or Klarna and standard credit products from Visa or Mastercard. Evaluating the total cost and personal financial habits ensures the optimal payment method, enhancing purchasing power without risking debt accumulation.

Buy Now, Pay Later (BNPL) vs Traditional Credit Infographic