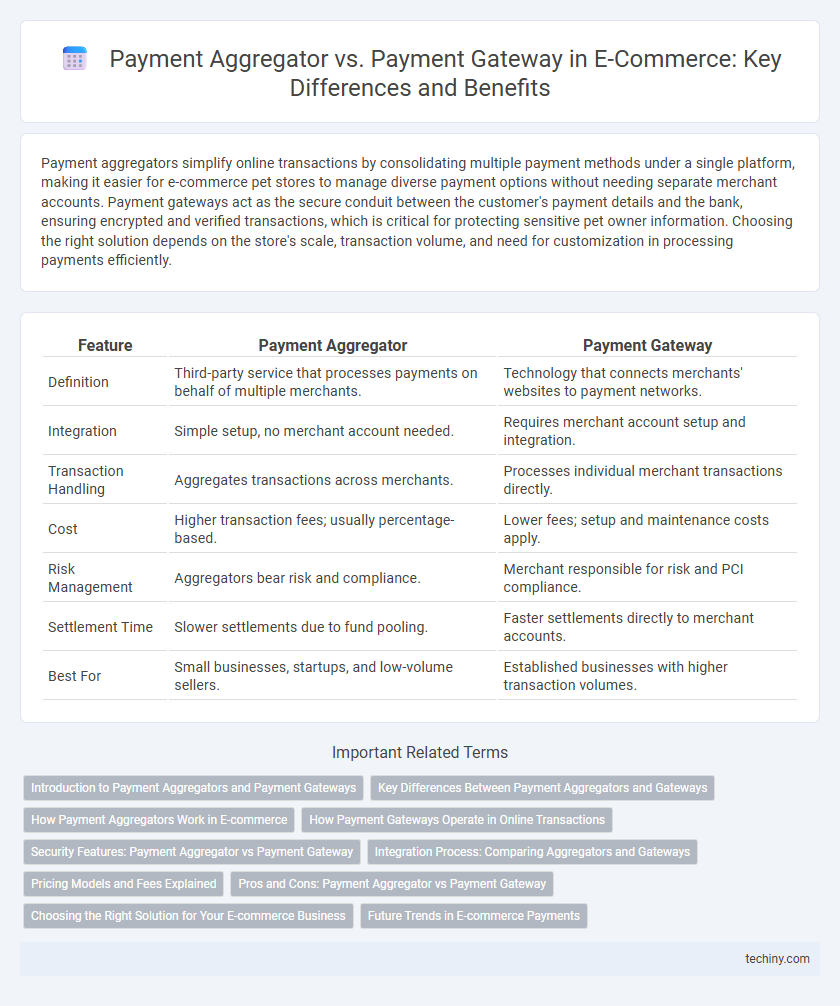

Payment aggregators simplify online transactions by consolidating multiple payment methods under a single platform, making it easier for e-commerce pet stores to manage diverse payment options without needing separate merchant accounts. Payment gateways act as the secure conduit between the customer's payment details and the bank, ensuring encrypted and verified transactions, which is critical for protecting sensitive pet owner information. Choosing the right solution depends on the store's scale, transaction volume, and need for customization in processing payments efficiently.

Table of Comparison

| Feature | Payment Aggregator | Payment Gateway |

|---|---|---|

| Definition | Third-party service that processes payments on behalf of multiple merchants. | Technology that connects merchants' websites to payment networks. |

| Integration | Simple setup, no merchant account needed. | Requires merchant account setup and integration. |

| Transaction Handling | Aggregates transactions across merchants. | Processes individual merchant transactions directly. |

| Cost | Higher transaction fees; usually percentage-based. | Lower fees; setup and maintenance costs apply. |

| Risk Management | Aggregators bear risk and compliance. | Merchant responsible for risk and PCI compliance. |

| Settlement Time | Slower settlements due to fund pooling. | Faster settlements directly to merchant accounts. |

| Best For | Small businesses, startups, and low-volume sellers. | Established businesses with higher transaction volumes. |

Introduction to Payment Aggregators and Payment Gateways

Payment aggregators provide a unified platform that allows e-commerce merchants to accept multiple payment methods without needing separate merchant accounts, simplifying transaction management. Payment gateways act as the secure technology that processes online payment transactions by encrypting sensitive card information and transmitting it from the customer to the acquiring bank. Both solutions are essential in e-commerce for facilitating seamless and secure payment processing, but payment aggregators bundle multiple gateway functionalities under a single service.

Key Differences Between Payment Aggregators and Gateways

Payment aggregators act as intermediaries allowing multiple merchants to process payments under a single account, while payment gateways serve as the technology that securely transmits transaction data from the merchant to the acquiring bank. Payment aggregators typically offer faster onboarding and lower setup costs, whereas payment gateways require individual merchant accounts and provide direct control over transactions. The key difference lies in ownership and control: aggregators consolidate funds in a pooled account, while gateways facilitate direct merchant-to-bank transactions for greater autonomy.

How Payment Aggregators Work in E-commerce

Payment aggregators in e-commerce streamline the transaction process by collecting payments from multiple buyers and settling them into a single merchant account, eliminating the need for merchants to establish individual accounts with multiple banks. They handle payment processing, fraud detection, and currency conversion, enabling seamless checkout experiences across various payment methods. By aggregating payments, these platforms reduce setup time and operational complexity, allowing small and medium-sized enterprises to efficiently accept online payments.

How Payment Gateways Operate in Online Transactions

Payment gateways securely capture and transmit customer payment information from an online store to the acquiring bank or payment processor, facilitating real-time authorization of transactions. They utilize encryption protocols such as SSL to ensure sensitive data like credit card numbers and CVV codes remain protected during the transaction process. Payment gateways also handle communication between the merchant, card networks, and banks, enabling seamless and secure payment approvals or declines in ecommerce environments.

Security Features: Payment Aggregator vs Payment Gateway

Payment aggregators provide consolidated security measures such as PCI DSS compliance, tokenization, and fraud detection to protect multiple merchants under a single platform. Payment gateways offer direct encryption protocols, multi-factor authentication, and secure socket layer (SSL) technology to ensure individual transaction security between merchants and customers. Both systems incorporate robust security features, but gateways typically enable more granular control over transaction data and risk management.

Integration Process: Comparing Aggregators and Gateways

Payment aggregators offer a simplified integration process by providing a single API that supports multiple payment methods, reducing the need for extensive technical setup. Payment gateways require individual integration with each payment provider, demanding more customization and developer resources. E-commerce businesses benefit from aggregators when seeking quick deployment, while gateways are preferred for tailored, scalable payment solutions.

Pricing Models and Fees Explained

Payment aggregators typically charge a fixed transaction fee combined with a small percentage of the payment amount, making them ideal for small to medium businesses with varying sales volumes. Payment gateways often involve setup fees, monthly maintenance costs, and per-transaction charges that vary based on payment methods and currency types, catering to enterprises requiring custom payment solutions. Understanding these pricing models helps merchants optimize cost-efficiency based on their sales size and transaction frequency.

Pros and Cons: Payment Aggregator vs Payment Gateway

Payment aggregators simplify the payment process by consolidating multiple payment methods under a single platform, reducing setup time and costs, but they may impose higher transaction fees and limited control over customer data. Payment gateways provide direct integration with merchant accounts, offering enhanced security, customization, and lower per-transaction costs, though they require more complex setup and ongoing maintenance. Choosing between payment aggregator and payment gateway depends on business scale, transaction volume, and the need for control versus convenience in payment processing.

Choosing the Right Solution for Your E-commerce Business

Choosing the right payment solution for your e-commerce business depends on transaction volume, customer experience, and integration complexity. Payment aggregators offer simplified onboarding and consolidated reporting ideal for small to medium businesses, while payment gateways provide direct payment processing and greater control suitable for larger enterprises with higher security demands. Understanding your business scale and technical capabilities ensures seamless transactions and optimized payment management.

Future Trends in E-commerce Payments

Payment aggregators are evolving to integrate AI-driven fraud detection and multi-currency support, enhancing seamless cross-border transactions in e-commerce. Payment gateways are adopting advanced encryption and tokenization technologies to improve security and reduce transaction latency, meeting growing consumer demands for faster checkout experiences. Both solutions are increasingly leveraging blockchain and biometric authentication to drive innovation and trust within the future landscape of digital payments.

Payment Aggregator vs Payment Gateway Infographic