ARIMA models are widely used for time series forecasting by capturing autocorrelations in stationary data through differencing, while SARIMA extends ARIMA by incorporating seasonal components to handle repeating patterns. SARIMA models provide improved accuracy for datasets with strong seasonal effects by integrating seasonal terms and differencing, making them suitable for complex time series with periodic fluctuations. Understanding the distinctions between ARIMA and SARIMA is essential for selecting the appropriate model based on the presence of seasonality in the data.

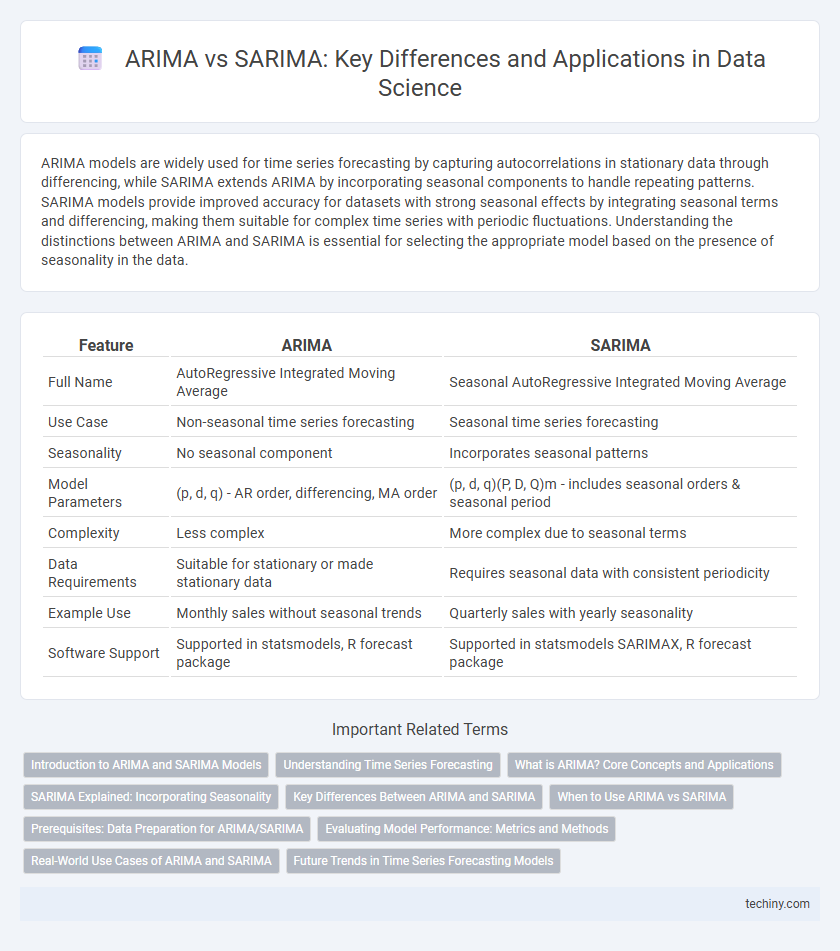

Table of Comparison

| Feature | ARIMA | SARIMA |

|---|---|---|

| Full Name | AutoRegressive Integrated Moving Average | Seasonal AutoRegressive Integrated Moving Average |

| Use Case | Non-seasonal time series forecasting | Seasonal time series forecasting |

| Seasonality | No seasonal component | Incorporates seasonal patterns |

| Model Parameters | (p, d, q) - AR order, differencing, MA order | (p, d, q)(P, D, Q)m - includes seasonal orders & seasonal period |

| Complexity | Less complex | More complex due to seasonal terms |

| Data Requirements | Suitable for stationary or made stationary data | Requires seasonal data with consistent periodicity |

| Example Use | Monthly sales without seasonal trends | Quarterly sales with yearly seasonality |

| Software Support | Supported in statsmodels, R forecast package | Supported in statsmodels SARIMAX, R forecast package |

Introduction to ARIMA and SARIMA Models

ARIMA (AutoRegressive Integrated Moving Average) models capture time series data patterns by combining autoregression, differencing to achieve stationarity, and moving average components, making them effective for forecasting non-seasonal data. SARIMA (Seasonal ARIMA) extends ARIMA by incorporating seasonal differencing and seasonal autoregressive and moving average terms, enabling it to model and forecast seasonal fluctuations in time series. Both models require parameter estimation (p,d,q for ARIMA and P,D,Q,m for SARIMA) to accurately reflect temporal dependencies and seasonal effects.

Understanding Time Series Forecasting

ARIMA models capture non-seasonal time series data by combining autoregression, differencing, and moving averages to forecast future points based on past values. SARIMA extends ARIMA by incorporating seasonal components, allowing it to model data with repeating patterns or seasonality effectively. Choosing between ARIMA and SARIMA depends on whether the time series exhibits seasonality, with SARIMA providing more accurate forecasts for seasonal datasets.

What is ARIMA? Core Concepts and Applications

ARIMA (AutoRegressive Integrated Moving Average) is a powerful statistical model used for analyzing and forecasting time series data by combining autoregression, differencing, and moving averages to capture various patterns. The core concepts include the autoregressive (AR) component, which models the relationship between an observation and previous values; the integrated (I) part, which involves differencing the data to achieve stationarity; and the moving average (MA) component, which captures the influence of past forecast errors. ARIMA is widely applied in economics, finance, and environmental studies for predicting trends, seasonal patterns, and cyclical changes in time-dependent datasets.

SARIMA Explained: Incorporating Seasonality

SARIMA models extend ARIMA by incorporating seasonal components, allowing for the modeling of both non-seasonal and seasonal patterns in time series data. By adding seasonal differencing and seasonal autoregressive and moving average terms, SARIMA effectively captures repetitive fluctuations occurring at fixed intervals, enhancing forecast accuracy. This seasonal integration makes SARIMA particularly useful for data exhibiting clear periodic behavior, such as monthly sales or quarterly revenue.

Key Differences Between ARIMA and SARIMA

ARIMA (AutoRegressive Integrated Moving Average) models capture non-seasonal time series data patterns through autoregression, differencing, and moving averages, whereas SARIMA (Seasonal ARIMA) extends ARIMA by incorporating seasonal components to handle periodic fluctuations. ARIMA models use parameters (p, d, q) representing autoregressive terms, integration order, and moving average terms, while SARIMA adds seasonal parameters (P, D, Q, m) to address seasonality with period length m. Key differences lie in SARIMA's ability to model both seasonal and non-seasonal data simultaneously, making it suitable for datasets with recurring seasonal patterns.

When to Use ARIMA vs SARIMA

Use ARIMA models for time series data exhibiting non-seasonal patterns with trends and autocorrelations, focusing on differencing to achieve stationarity. SARIMA models are optimal for datasets with strong seasonal effects, integrating seasonal differencing and periodic components to capture recurring patterns. Choose SARIMA over ARIMA when seasonal fluctuations significantly impact forecast accuracy.

Prerequisites: Data Preparation for ARIMA/SARIMA

Effective data preparation for ARIMA and SARIMA models requires stationarity, achieved through differencing or transformation to stabilize mean and variance over time. Both models demand thorough identification of seasonality patterns and lag structures to capture data dependencies, with SARIMA extending ARIMA by incorporating seasonal differencing and seasonal autoregressive and moving average terms. Ensuring data is free of missing values and outliers is essential to enhance model accuracy and forecasting reliability in time series analysis.

Evaluating Model Performance: Metrics and Methods

Evaluating the performance of ARIMA and SARIMA models relies heavily on metrics such as Mean Absolute Error (MAE), Root Mean Square Error (RMSE), and Akaike Information Criterion (AIC) to quantify forecast accuracy and model fit. Time series cross-validation and rolling forecast origin methods provide robust frameworks for assessing out-of-sample predictive performance, critical for models capturing seasonality in SARIMA. Comparing residual diagnostics like autocorrelation function (ACF) plots helps ensure that SARIMA better addresses seasonal patterns, often yielding improvements over non-seasonal ARIMA models in performance metrics.

Real-World Use Cases of ARIMA and SARIMA

ARIMA models are extensively applied in financial market forecasting, inventory management, and demand prediction where data exhibit non-seasonal trends, enabling accurate short-term forecasting through differencing and autoregressive components. SARIMA expands ARIMA's capabilities by incorporating seasonal patterns, making it the preferred choice in retail sales analysis, energy consumption forecasting, and climate data modeling where periodic fluctuations critically influence data behavior. Organizations leverage ARIMA for stable, non-seasonal time series, while SARIMA is optimal for datasets with clear seasonal cycles to improve forecast precision and operational decision-making.

Future Trends in Time Series Forecasting Models

ARIMA models provide robust forecasting for stationary time series but often struggle with seasonal patterns, whereas SARIMA extends ARIMA by integrating seasonal differencing and seasonal parameters for improved accuracy. Future trends in time series forecasting emphasize blending SARIMA with machine learning techniques to enhance model adaptability and predictive performance in complex data environments. Advances in hybrid models and automated hyperparameter tuning are expected to drive greater precision and efficiency in forecasting financial markets, climate data, and demand planning.

ARIMA vs SARIMA Infographic